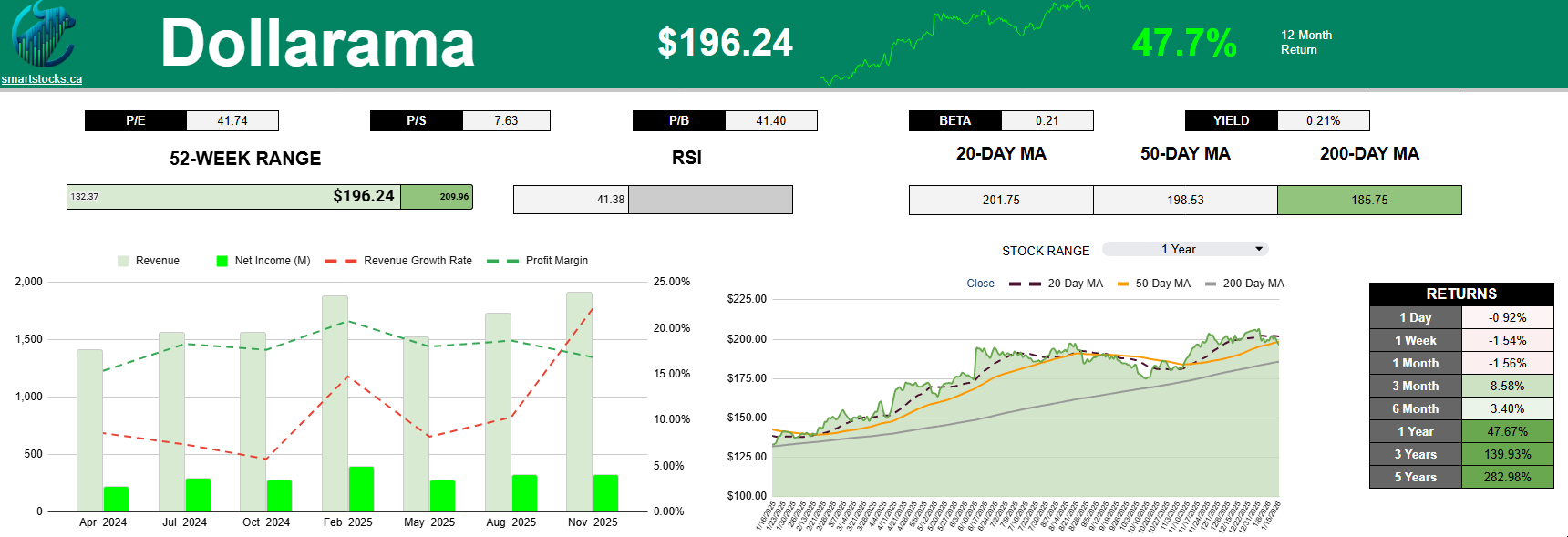

Dollarama (TSX:DOL) has been a cornerstone of Canadian growth portfolios for years, delivering a nearly 300% return over the past five fiscal years. While the company continues to benefit from strong consumer demand and a 6% rise in comparable store sales, the stock has stumbled with a 4% decline to open 2026. This recent dip raises questions about whether the retailer is finally facing a valuation ceiling after reaching a market capitalization of 54 billion dollars.

Key Numbers

- 5-year share appreciation: 280%

- Current market capitalization: $54 billion

- Year-to-date performance: -4%

- Recent comparable sales growth: 6%

- Trailing price-to-earnings ratio: 42

Dollarama’s growth has been impressive

The retail chain has demonstrated remarkable resilience, expanding its transaction volume and average spend even as shoppers tighten their belts. Its dominance in the Canadian value retail space has allowed it to maintain a 54 billion dollar market cap, though the 4% decline since January suggests that investors may be growing cautious. Despite the solid fundamentals and continued expansion, the stock’s momentum appears to be cooling as the market evaluates its high entry price.

The stock’s valuation remains a concern

The primary hurdle for new investors is the company’s valuation, which currently sits at 42 times trailing earnings. A multiple this high demands exceptional and consistent growth, leaving little room for error if economic conditions shift or consumer spending patterns change. While the business itself remains a high-quality operation, the premium price tag may lead to further stagnation or price corrections in the coming months.

Given the current pricing, the stock may see additional downward pressure as the market seeks a more reasonable valuation. For now, a patient approach is likely the best strategy until the share price better reflects the company’s underlying earnings growth.

Dollarama remains a premier choice for long-term growth investors, though at its current premium, it is best suited for those with a high tolerance for valuation risk or those waiting for a deeper pullback.