When it comes to saving and investing in Canada, two of the most popular registered accounts are the Tax-Free Savings Account (TFSA) and the Registered Retirement Savings Plan (RRSP). Both accounts offer unique tax advantages that can help you grow your money faster than in a regular, taxable account. But the question many Canadians ask is: which one should I invest in first?

Let’s break down the differences, benefits, and drawbacks of each, and explore which type of investor might prefer one account over the other.

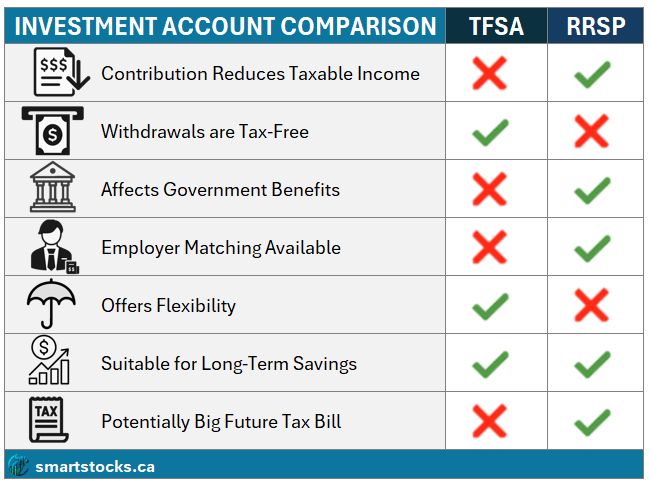

What Is a TFSA?

The TFSA was introduced in 2009 to encourage Canadians to save more. Every year, you get a set contribution limit (in 2025, it’s $7,000), and unused room carries forward indefinitely. If you’ve never contributed and were at least 18 in 2009, your total TFSA room as of 2025 is $102,500.

The big advantage of a TFSA is that all growth inside the account is tax-free. Whether you earn interest, dividends, or capital gains, you won’t owe a penny in taxes when you withdraw. You can also take out money at any time, for any purpose, and the withdrawn amount gets added back to your room the following year.

Drawback: Contributions are not tax-deductible. That means putting money into a TFSA won’t lower your taxable income the way RRSP contributions do.

What Is an RRSP?

The RRSP is designed to help Canadians save specifically for retirement. Your contribution limit is 18% of your previous year’s income, up to an annual maximum ($32,490 for 2025). Unused room also carries forward.

The key benefit of an RRSP is that contributions are tax-deductible. For example, if you earn $70,000 and contribute $10,000, you’ll only be taxed on $60,000 of income. That deduction could save you roughly $2,000–$3,500 in taxes, depending on your province and marginal tax rate. Higher-income earners benefit the most — someone making $120,000 who contributes $10,000 could see a tax savings of $4,000 or more. Inside the account, your investments grow tax-deferred, meaning you won’t pay taxes until you withdraw the money in retirement, ideally when you’re in a lower tax bracket.

Drawback: Withdrawals are fully taxable as income, and pulling money early can come with withholding taxes and long-term tax consequences. Unlike a TFSA, you don’t automatically regain contribution room after a withdrawal (with the exception of specific programs like the Home Buyers’ Plan or Lifelong Learning Plan).

Example RRSP Tax Savings in 2025

By contributing to an RRSP, you get immediate tax savings. And the higher your income bracket, the larger the potential savings there can be from the tax deduction:

| Annual Income | RRSP Contribution | Approx. Marginal Tax Rate | Estimated Tax Savings |

|---|---|---|---|

| $50,000 | $10,000 | ~29% | $2,900 |

| $75,000 | $10,000 | ~34% | $3,400 |

| $100,000 | $10,000 | ~38% | $3,800 |

| $150,000 | $10,000 | ~43% | $4,300 |

Why This Matters

- Higher incomes = bigger savings: The more you earn, the higher your marginal tax rate, and the more valuable your RRSP deduction becomes.

- Refund or reduced tax bill: That savings comes back to you as either a bigger tax refund or less owing when you file your return.

- Strategic timing: Some Canadians even delay claiming their RRSP deduction until a future year when their income (and tax rate) is higher, maximizing the refund.

Employer RRSP contributions could give you an extra incentive

Another important factor to consider with RRSPs is the possibility of employer matching through a group RRSP or pension plan. Many Canadian employers will contribute to an employee’s RRSP when the employee does, often matching contributions dollar-for-dollar up to a certain percentage of salary. This essentially amounts to “free money,” and it can significantly outweigh the tax advantages of a TFSA. For example, if you contribute $5,000 to your group RRSP and your employer matches that with another $5,000, you’ve instantly doubled your contribution before investment growth or tax refunds are even factored in.

This employer match can easily tip the scales in favour of the RRSP, even if you’re in a lower tax bracket now or expect to be in a higher one later. The added contributions provide a boost that no TFSA can replicate, and when combined with the upfront tax refund, the RRSP becomes a very compelling savings vehicle. The key trade-off is that your money is generally locked into retirement savings, and you’ll face the usual tax consequences on withdrawals. But if your employer offers matching, it’s often wise to take full advantage of it before prioritizing TFSA contributions.

What If I have to withdraw from an RRSP before retirement?

Withdrawing early from an RRSP comes with several significant drawbacks. Any withdrawal is immediately subject to a withholding tax of 10%–30%, depending on the amount, and the entire sum is treated as taxable income in that year. This can push you into a higher tax bracket and create a larger-than-expected bill at tax time. Perhaps even more importantly, the contribution room you used is gone forever — you cannot re-contribute that withdrawn amount in the future. Beyond taxes, early withdrawals can also reduce your eligibility for income-tested government benefits such as the Canada Child Benefit or Old Age Security in retirement, making the impact of pulling funds from your RRSP more severe than it first appears.

By contrast, the TFSA offers much greater flexibility. Withdrawals can be made at any time, for any reason, and they are completely tax-free. Unlike the RRSP, amounts withdrawn from a TFSA are added back to your contribution room at the start of the following year, meaning you can re-contribute without penalty. Because TFSA withdrawals are not considered taxable income, they also do not affect your tax bracket or your eligibility for government benefits. This flexibility makes the TFSA particularly well-suited for shorter-term savings goals or situations where access to funds may be needed before retirement, while the RRSP is best reserved for money you can leave untouched until later in life.

Which Investors Should Choose Which?

- TFSA: Best for young investors, low-to-moderate income earners, or anyone saving for flexible goals (like a home, car, or emergency fund). Since contributions don’t affect taxable income, TFSAs shine when your income — and tax bracket — is still relatively low. They’re also the safer account to max out first, because funds can be withdrawn tax-free and re-contributed later, making them useful for both emergencies and shorter-term planning.

- RRSP: Better suited for higher-income earners who want to reduce taxable income today. If you’re in a high tax bracket, the immediate deduction from RRSP contributions can be a big win. However, while you may ultimately come out ahead if you retire in a lower tax bracket, RRSP withdrawals can still generate a large tax bill — and if you need to take out a lump sum at once, it may come at an inopportune time. Spacing withdrawals over multiple years can help, but not everyone has the flexibility to do so. This makes it critical to treat RRSPs as long-term retirement savings rather than short-term vehicles.

- Combination Approach: Many Canadians benefit from using both. A TFSA provides flexibility and tax-free withdrawals for shorter-term needs, while an RRSP builds a retirement nest egg with upfront tax savings. For those with employer matching on RRSP contributions, it often makes sense to prioritize that first, and then turn to the TFSA. Ultimately, the best strategy depends on your income level, tax situation, and savings goals — but a mix of the two accounts ensures you get the tax advantages of both flexibility and long-term compounding.